The Legal500 Comparative Guides aim to be a valuable tool for in-house lawyers worldwide. In the 2026 guide, Ioannides Demetriou LLC Partners Christina Ioannidou and Katerina Hadjichristofi contributed to the Cyprus – Project Finance chapter. This country-specific Q&A provides an overview of project finance laws and regulations applicable in Cyprus.

December 2025: Reflecting on the evolving Cyprus real estate legal landscape and the opportunities it presents for investors, professionals, and clients alike.

The Legal500 Country Comparative Guide on Cyprus Real Estate offers an insightful snapshot of a market underpinned by a solid and transparent legal framework – one that continues to anchor investor confidence and drive growth across residential, commercial and tourism-related sectors.

As we look ahead to 2026, these insights not only reflect current trends but also help chart a course for thoughtful decision-making in an increasingly dynamic environment.

A notable win for Ioannides Demetriou LLC: The Supreme Court of Cyprus Opens the Door to Further Evidence on Appeal

It doesn’t happen very often. In fact, it arises only in truly exceptional circumstances and under the strict conditions established by case law. Yet on December 3rd, 2025, the Supreme Court of Cyprus took the uncommon step of allowing the admission of further evidence in the course of Civil Appeal No. 189/2017.

It is a well-established principle that in ordinary litigation, the rights of the parties are assessed on the facts of each case, as these are presented to the first-instance court. As a result, an appellate court will generally allow very little room for the introduction of new evidence.

Both English and Cypriot case-law recognise that departure from this general rule is justified only when specific criteria are met. These include that the evidence sought to be introduced on appeal (i) could not, with reasonable diligence, have been obtained for use at the trial stage; (ii) is of such significance that it would probably have a material impact on the outcome, although not necessarily decisive; and (iii) appears to be credible on its face, although it need not be incontrovertible.

Turning to the facts of the above-mentioned Appeal, the case considered an appeal to the judgment of the first-instance Court where it was decided that the Claimants of the two consolidated Actions were entitled to their share in two Trust Funds. A primary and fundamental requirement for a person to be considered a beneficiary of the Trusts Funds was that they were registered shareholders of a public Czech company at the time the Trusts were created. The Court, finding that the said requirement was satisfied, ruled in favor of the Claimants and awarded them specific amounts. Remarkably enough, the first-instance Court, although granting judgment in favour of the Claimants, clarified in various points of the judgment that any involvement of the Claimants in unlawful activities could constitute a ground preventing them from receiving their entitlement from the trust funds.

Nevertheless, the Defendant, being the trustee of the Trust funds disagreed with this decision and filed the above-mentioned Civil Appeal.

While the said appeal was still pending, and in early October 2022, the Court of Czech Republic issued a final judgment by which it was decided that the Claimants had never lawfully acquired the shares they held in the Czech company, and that the actions through which the Claimants obtained those shares were entirely and ab initio void.

Following the issuance of the Czech judgment, the Defendant filed the present application for the submission of further evidence before the Supreme Court, seeking to submit as evidence the said Czech judgement, as well as legal opinions and certificates from Czech lawyers concerning the finality of the judgment and the progress of the judicial proceedings.

The Supreme Court, finding that the conditions for the submission of further evidence were satisfied, and relying on the findings of the first-instance court according to which any involvement of the Claimants in unlawful activities could prevent them from receiving their entitlement from the trust funds, allowed the application.

By permitting the submission of further evidence, the Supreme Court not only acknowledged the exceptional circumstances of the case but also reinforced the principle that it may depart from ordinary course of proceedings if necessary.

For anyone following developments in Cypriot law, this case is definitely a striking reminder that the Court can, when appropriate, go beyond standard procedures if justice so requires.

12 December 2025, Nicosia: Ioannides Demetriou LLC Chairman, Pambos Ioannides, awarded at the KEBE Cyprus Chamber of Commerce and Industry 2025 Business Leader Awards

IOANNIDES DEMETRIOU LLC partners and members are honoured to announce that our Chairman Mr. Pambos Ioannides has been selected to receive the 2025 Business Leader Award for Financial and Professional Services of the Cyprus Chamber of Commerce and Industry.

The award is presented by the CCCI in collaboration with IMH to the individual who has demonstrated exemplary business leadership, outstanding performance, and excellence in their field, in recognition of their significant contributions to the Cypriot business community.

The award was granted on 11.12.2025 at an exclusive ceremony in the presence of the President of the House of Representatives and other senior Government officials.

As our firm welcomes this recognition, we extend our gratitude to our clients and collaborators for their continued trust. We remain committed to excellence and the delivery of outstanding services.

“Join us a father–son duo of lawyers for a conversation about the best and worst experiences in transition from the senior to the new generation.”

Andrew Demetriou and Theo Demetriou take the stage at Inspire 2025 for a candid, honest and, possibly, humorous conversation on what it really takes to navigate transition across generations in a leading law firm that has an “open door” policy on partnership admissions.

“There’s no perfect moment for succession. There’s only the moment when the past, the present, and the future sit at the same table or rather… step onto the same stage.”

INSPIRE 2025 THE A-Z OF ENTREPRENEURSHIP

About:

In a world that changes faster than ever, where uncertainty is the only certainty, and where bold visionaries shape tomorrow’s reality – Cyprus rises as a hub of opportunity, innovation, and entrepreneurial excellence.

On the 25th and 26th of September 2025, the heart of Nicosia will pulse with energy, ideas, ambition, and celebration. Makarios Avenue and its surrounding spaces will be transformed into a vibrant living lab of entrepreneurial culture, where creativity meets business, and experience meets aspiration.

This is not just a festival. It’s a two-day immersive journey into the stories, strategies, setbacks, and successes that shape the world of business – from start-up grit to boardroom leadership, from local family businesses to global industry titans.

Στις 16/4/2025 το Ανώτατο Δικαστήριο του Ηνωμένου Βασίλειου – UK Supreme Court – εξέδωσε μια πολύ σημαντική απόφαση.

Το αντικείμενο της απόφασης αυτής δεν ήταν άλλο παρά η ορθή ερμηνεία της έννοιας των όρων «άνδρας», «γυναίκα» και «φύλο» στον Νόμο περί Ισότητας του 2010 («EA 2010»)

Cyprus has emerged into a leading investment funds centre in Europe offering direct access to key markets. The island is an ideal investments gateway into the European Union and a portal for investments outside the EU, particularly into the Middle East and India. Cyprus’ competitive advantages are further enriched by a robust and transparent legal and regulatory framework and a versatile tax regime.

OUR ADDED VALUE ADVISORY SERVICES We can assist in designing and implementing the most efficient tax and operational fund structure, to best accommodate your requirements and goals. We will advise and oversee on legal, regulatory, taxation, administration and secretarial matters and we will provide ongoing assistance on corporate governance and business matters of importance.

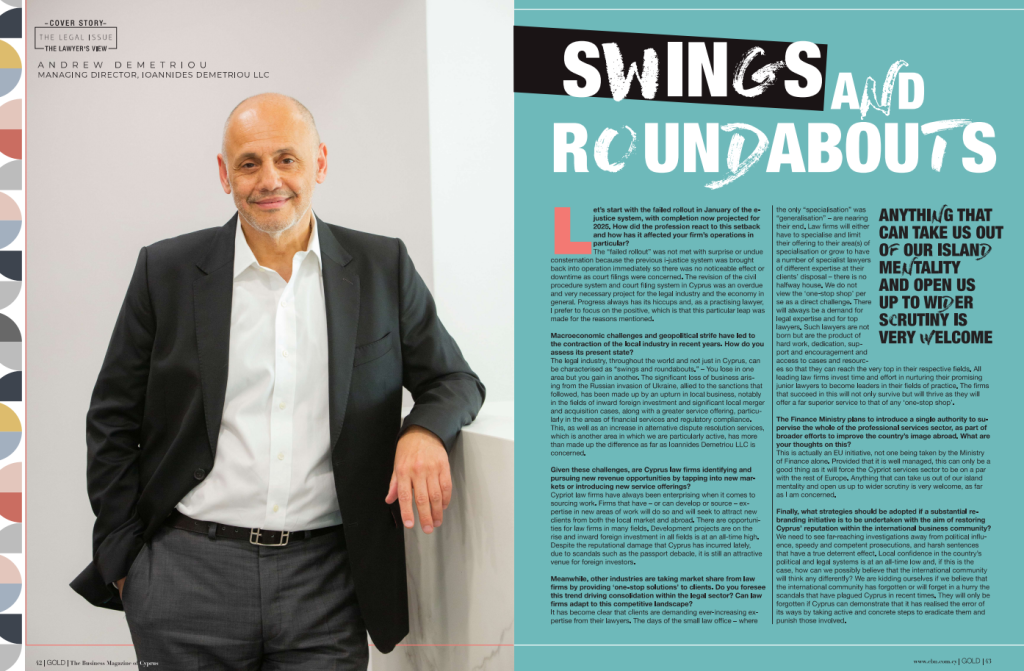

Let’s start with the failed rollout in January of the e-justice system, with completion now projected for 2025. How did the profession react to this setback and how has it affected your firm’s operations in particular?

The “failed rollout” was not met with surprise or undue consternation because the previous i-justice system was brought back into operation immediately so there was no noticeable effect or downtime as court filings were concerned. The revision of the civil procedure system and court filing system in Cyprus was an overdue and very necessary project for the legal industry and the economy in general. Progress always has its hiccups and, as a practising lawyer, I prefer to focus on the positive, which is that this particular leap was made for the reasons mentioned.

Macroeconomic challenges and geopolitical strife have led to the contraction of the local industry in recent years. How do you assess its present state?

The legal industry, throughout the world and not just in Cyprus, can be characterised as “swings and roundabouts.” – You lose in one area but you gain in another. The significant loss of business arising from the Russian invasion of Ukraine, allied to the sanctions that followed, has been made up by an upturn in local business, notably in the fields of inward foreign investment and significant local merger and acquisition cases, along with a greater service offering, particularly in the areas of financial services and regulatory compliance. This, as well as an increase in alternative dispute resolution services, which is another area in which we are particularly active, has more than made up the difference as far as Ioannides Demetriou LLC is concerned.

Given these challenges, are Cyprus law firms identifying and pursuing new revenue opportunities by tapping into new markets or introducing new service offerings?

Cypriot law firms have always been enterprising when it comes to sourcing work. Firms that have – or can develop or source – expertise in new areas of work will do so and will seek to attract new clients from both the local market and abroad. There are opportunities for law firms in many fields. Development projects are on the rise and inward foreign investment in all fields is at an all-time high. Despite the reputational damage that Cyprus has incurred lately, due to scandals such as the passport debacle, it is still an attractive venue for foreign investors.

Meanwhile, other industries are taking market share from law firms by providing ‘one-stop solutions’ to clients. Do you foresee this trend driving consolidation within the legal sector? Can law firms adapt to this competitive landscape?

It has become clear that clients are demanding ever-increasing expertise from their lawyers. The days of the small law office – where the only “specialisation” was “generalisation” – are nearing their end. Law firms will either have to specialise and limit their offering to their area(s) of specialisation or grow to have a number of specialist lawyers of different expertise at their clients’ disposal – there is no halfway house. We do not view the ‘one-stop shop’ per se as a direct challenge. There will always be a demand for legal expertise and for top lawyers. Such lawyers are not born but are the product of hard work, dedication, support and encouragement and access to cases and resources so that they can reach the very top in their respective fields. All leading law firms invest time and effort in nurturing their promising junior lawyers to become leaders in their fields of practice. The firms that succeed in this will not only survive but will thrive as they will offer a far superior service to that of any ‘one-stop shop’.

The Finance Ministry plans to introduce a single authority to supervise the whole of the professional services sector, as part of broader efforts to improve the country’s image abroad. What are your thoughts on this?

This is actually an EU initiative, not one being taken by the Ministry of Finance alone. Provided that it is well managed, this can only be a good thing as it will force the Cypriot services sector to be on a par with the rest of Europe. Anything that can take us out of our island mentality and open us up to wider scrutiny is very welcome, as far as I am concerned.

Finally, what strategies should be adopted if a substantial rebranding initiative is to be undertaken with the aim of restoring Cyprus’ reputation within the international business community?

We need to see far-reaching investigations away from political influence, speedy and competent prosecutions, and harsh sentences that have a true deterrent effect. Local confidence in the country’s political and legal systems is at an all-time low and, if this is the case, how can we possibly believe that the international community will think any differently? We are kidding ourselves if we believe that the international community has forgotten or will forget in a hurry the scandals that have plagued Cyprus in recent times. They will only be forgotten if Cyprus can demonstrate that it has realised the error of its ways by taking active and concrete steps to eradicate them and punish those involved.

Client Alert: IOANNIDES DEMETRIOU LLC, acting on behalf of the Electricity Authority of Cyprus, has secured a victory of pivotal significance to our client and the electricity market of Cyprus in general before the Court of Appeal (Administrative Division).

The judgment in Appeals 13/2024 and 14/2024, handed down on the 18.7.2024, reverses the first instance judgment of the Administrative Court and paves the way for the signature of the contract between the Electricity Authority of Cyprus and the Cyprus Telecommunications Authority (CYTA) for the installation of 400,000 smart electricity meters all over Cyprus.

This project, valued at approximately EURO 50million, is a highly significant project as it represents a major and long awaited first step in the opening of the electricity market as well as the advent of the smart grid in Cyprus. Additionally, the introduction of a first roll out of 400,000 electricity smart meters will allow EAC and consumers to obtain electricity consumption data in real time. This translates to cost savings, improved efficiency, better planning and forecasting in relation to energy consumption and a host of other advantages the Cypriot consumer can benefit from.

The three lawyers involved in the matter from the outset on the part of our firm were our Managing Director, Andrew Demetriou and senior members of our Administrative law team, namely Partner Mrs. Anna Christou and Associate Director Mr. Demetris Kailis.

Pictured above at the signing ceremony of the contract between EAC and CYTA on 24.7.2024, from left to right, is the General Manager of EAC Mr. Adonis Yiasemides, the President of the Board of EAC Mr. George Petrou, the President of the Board of CYTA Mrs. Maria Tsiakka Olympiou, the Minister of Energy of the Republic of Cyprus Mr. George Papanastasiou and the Director General of the Ministry of Energy Mr. Marios Panayides.

The landscape of work has undergone significant transformation in recent years, which was particularly accelerated by the global pandemic. Teleworking has become increasingly common, prompting the need for a clear legislative framework to govern its implementation. This need has been addressed with the House of Representatives’ approval of a comprehensive framework regulating remote working. The Framework for Telework of 2023 Legislation (the “Law”), which came into effect on December 1, 2023, aims to establish guidelines and protections for both employers and employees navigating the remote work environment.

The Law stipulates that teleworking can be implemented under the following circumstances: (i) an optional teleworking scheme may be adopted subject to a written agreement entered into between the employer and the employee, (ii) mandatory teleworking may be imposed under a Decree issued by the Minister of Health due to public health considerations and (iii) mandatory teleworking may be required for an employee whose health is demonstrably at risk, which can be mitigated by refraining from working on the employer’s premises.

Apart from prescribing the conditions under which teleworking can be established, the Law also delineates the responsibilities that the employer bears towards the employee. Firstly, among these obligations is the coverage of expenses incurred by the employee related to teleworking. These expenses include various aspects, such as equipment costs (unless agreed to utilize the employer’s equipment), telecommunications, usage of the home workspace, and the maintenance and repair of equipment. Moreover, the employer bears the responsibility of ensuring that the employee receives the essential technical support required for their work. To further regulate the financial aspects, the Minister of Labour and Social Insurance is expected to issue a Decree specifying the minimum teleworking cost payable to the employee. Importantly, the Law stipulates that any expenses covered by employers will not be considered as part of the employee’s remuneration, but they are deemed as deductible expenses, exempted from both social insurance and taxation.

In maintaining consistency with the aforementioned responsibilities, the employer is obliged, among other things and in addition to those outlined in the Occupational Safety and Health Law 1996 to (i) have at their disposal a suitable and sufficient written risk assessment of the existing teleworking risks, (ii) determine the preventive and protective measures to be taken based on the written risk assessment, (iii) provide such information, instructions, and training to ensure the safety and health of their employees. Employers have the same health and safety responsibilities for employees, whether they work from home or in a workplace.

Furthermore, the Law requires that employers should provide certain information to employees regarding teleworking, within eight (8) days from the date of commencement of such arrangement. This information includes: a) The employee’s right to disconnect; b) An analysis of the extend of teleworking costs incurred by the employer; c) The equipment necessary for the provision of services remotely and the procedures in place for the technical support, maintenance and repair of the equipment; d) Any restrictions on the use of the equipment and any penalties in case of violation of the restrictions; e) The agreement regarding remote readiness, it’s time limits and the response deadlines of the teleworking employee; f) An evaluation of the risks associated with remote work and measures taken by the employer for their prevention based on the risk assessment; g) The responsibility to protect and secure the professional and personal data of the teleworking employee and the relevant procedure to comply with such obligation; h) The supervisor from whom the teleworker will receive instructions.

Any information which does not have to be personalised and addressed to teleworking employees, can be communicated to appropriate personnel through the employer’s internal policies.

Employees engaged in teleworking have the equivalent rights and obligations as their counterparts working on-site at the employer’s premises, including rights or obligations concerning their workload, assessment criteria and procedures, compensation, access to employer-related information, training, professional development, and where applicable trade union activity including their unhindered and confidential communication with trade union representatives.

A key protection established by the Law is the employees’ right to disconnect in order for the provisions of the Transparent and Predictable Working Conditions Law to be implemented. Employers and employees’ representatives are required to agree on the technical and organizational methods to ensure that remote employees can disconnect from electronic communication without any adverse consequences. If no such agreement is reached, employers must still notify employees of this right. Moreover, the Law also sets out the duties and powers of Inspectors, who are officials of the Ministry and/or other public servants appointed by the Minister of Labour and Social Insurance. Their primary responsibility is to ensure the thorough and effective enforcement of the provisions of the Law. Failure to comply with the provisions of the Law could render employers liable, with potential fines upon conviction not exceeding €10.000.

In conclusion, the Framework for Telework of 2023 represents a significant step towards formalizing and protecting the evolving landscape of remote work. This legislation not only establishes clear guidelines and responsibilities for both employers and employees but also ensures a fair and supportive environment for teleworking. By addressing key aspects such as expense coverage, health and safety requirements, and the right to disconnect, the Law aims to create a balanced framework that promotes productivity while safeguarding employee well-being. As teleworking becomes an integral part of the modern work environment, the effective implementation and adherence to this framework will be crucial in fostering a sustainable and equitable remote working culture.

Associated with

This website uses cookies to give you the best user experience, for analytics, and improvement of functionalities.

By using this site you agree to these cookies being set. To find out more see our Cookies and Privacy Policy.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.